|

|

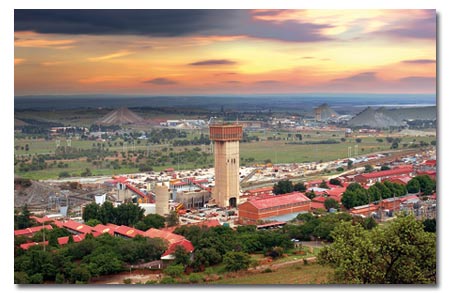

Vue générale de l'exploitation

![]()

Vergenoeg

Fluorspar Mine Site name

Vergenoeg Fluorspar Mine |

Vue de la mine en Janvier 2007

|

Fluorite sur Goethite |

a 30cm vug lined with stalictitic transluscent fluorite which is on iridesccent goethite |

![]()

MIXED

FORTUNES FOR FLUORSPAR

South Africa has about 10% of the world’s fluorspar reserves, but

its two principal producers have been experiencing mixed fortunes. Early

in 2007, the Spain’s Minerales y Productos Derivados SA (Europe’s

largest fluorspar user), invested R100 million in South African mining

junior Metorex Ltd and it is providing technical assistance for its Vergenoeg

fluorspar mine.

Metorex has been involved in a study into the possibility of establishing

an aluminium fluoride plant at Richards Bay to supply nearby aluminium

producers who currently import their fluoride needs. If the plant gets

the go-ahead, Vergenoeg’s annual production of fluorspar will increase

60,000-80,000 t/y from its current 180,000 t/y. Metorex’s principal

interest is supplying fluorspar to the new plant.

In contrast to Vergenoeg, which provides Metorex with some 15% of its

revenue at present, the Buffalo mine owned by Sallies Ltd has been plagued

wth difficulties. Some years ago Sallies tried, unsuccessfully, to renegotiate

a loss-making fixed-price supply contract with Honeywell. In good years,

when mining operations are not hampered by rains, Buffalo and the company’s

Witkop mine produce 200,000 t of fluorspar; about 5% of world demand.

Sallies and Honeywell have taken their dispute to international arbitration.

Meanwhile, Sallies posted a loss of R19,033 million last year.

source : http://www.mining-journal.com

![]()

South

Africa struggles with domestic issues

( 14 Sep 2007)

The ARM Two Rivers platinum mine

Though plagued by high death rates, power shortages, uncertainty due to

new laws and a move towards black empowerment, South Africa’s vibrant

mining industry is still surviving

THE South African government’s legislative programme to enforce the

Black Economic Empowerment initiative continues to cause controversy in

the country’s strong mining industry. By 2014, 26% of the country’s

mining industry has to be in black hands and mining companies have to

satisfy authorities that they are making progress towards empowerment

compliance if their rights to mine mineral resources are to be renewed.

A bill that would nationalise environmental standards and other aspects

of the current law is currently being debated in parliament, but the mining

industry has expressed serious reservations about one proposed clause.

This clause is designed to protect black empowerment investors with minority

stakes in mining companies and ensure that the black owners play active

rather than pass-ive roles in the mining industry. It would oblige mining

companies to seek ministerial approval of any sales, no matter how small,

of mining or prospecting rights.

Prior to the amendment bill, mining companies only needed to seek ministerial

approval for the disposal of a controlling interest in a mine. The bill

has taken four years to reach parliament, with hopes that it will soon

be passed.

Safety has become an overriding issue for a government that is determined

to restructure the mining industry by placing more power and control in

black hands. Minerals & Energy Minister Buyelwa Sonjica has criticised

the high number of death rates and companies have responded by closing

operations for several days to investigate accidents.

White mining executives have also come in for government criticism, with

ministerial allegations that their commitment to Black Economic Empowerment

is not wholehearted. Tension has also arisen between the government and

some mining sectors over the government’s insistence on greater domestic

beneficiation of South Africa’s export minerals.

On top of this, the country urgently needs new electricity-generating

capacity. The debate is whether more thermal stations will be built, with

their attendant CO2 emission problems, or whether to opt for a new generation

of nuclear plants.

Despite these issues, the underlying picture in South Africa remains relatively

unaltered. Gold production remains in decline as many mines are approaching

the end of their working life; platinum output continues to expand on

the back of rising global, industrial demand for the metal; coal and iron

ore exports remain affected by rail capacity; and production of ore from

metals including chrome, uranium and manganese is responding to growing

export demand.

CHROME SHORTAGES FORCE INPORTS

South Africa, which has more than two-thirds of the world’s chromite

reserves and supplies some 45% of the world’s ferrochrome, has, ironically,

had to import Indian ore for smelting during the first half of this year.

Samancor Ltd , the world’s largest ferrochrome producer imported

more than 80,000 t of lumpy ore to add to its own 300,000 t domestic mine

capacity. Major expansion programmes by the country’s ferrochrome

smelters have threatened further to outstrip domestic ore availability.

Almost simultaneously, several smelters were obliged to feed power back

into the national grid during this year’s South African winter as

the country approached the limits of its generating capacity, a capacity

constraint that had led to power cuts for domestic and industrial users.

Government policy is that mineral producers should curtail their exports

of raw ores and beneficiate raw materials within South Africa itself.

Expansion projects are characterised by the plans of International Ferro

Metals Ltd (IFM) to add three furnaces to its existing two, which will

add 400,000 t by 2010 to the company’s existing 267,000 t of annual

ferrochrome capacity. Although international ferrochrome prices have increased

on rising demand from China and, as Russia and Kazakhstan have curtailed

spot sales to Europe, the persistent strength of the South African rand

and the soaring capital cost of constructing new furnaces have led some

South African producers to re-examine some of their expansion plans.

Furnace builder Pyromet has been said to have almost doubled the price

of its new furnaces. Ferrochrome contract prices, which are negotiated

quarterly, rose from US$0.75/lb in the first quarter of 2007 to at least

US$1/lb in the second quarter. Further increases have been predicted when

third-quarter prices are set in September.

CAPACITY RESTRICTS COAL EXPORTS

Along with other South African bulk commodity producers, coal exporters

are being restricted by capacity constraints. Richards Bay Coal Terminal

(RBCT) is expanding operations from 72 Mt/y to 91 Mt/y. A major snag,

however, could be the willingness of state-owned rail operator Transnet

to increase rail capacity between the coal-fields of Mpumalanga Province

and Richards Bay.

As it is, some major coal producers, such as BHP Billiton, have been selling

their export entitlements to black empowerment companies favoured by government.

BHP Billiton has already sold a 1 Mt export entitlement to black empowerment

company Exxaro Resources Ltd, and said earlier this year that it wanted

to divest a further 6 Mt.

Exxaro itself sprang from the sale of coal interests by Anglo Coal and

has been on the acquisition trail since then, attempting to fulfil its

ambition to become South Africa’s largest producer by 2012. Its principal

expansion hopes lie in the development of the Waterberg coal-fields near

South Africa’s eastern border with Botswana where reserves have the

potential to become the country’s largest coal-producing region within

20 years.

On the domestic front, the country has an urgent need for additional electricity-generating

capacity. No new thermal-power stations have been built by Eskom, the

state-owned power utility, for the past 20 years and demand for domestic

power has grown beyond expectations. Whether new power stations, which

have a life expectancy of decades, will be thermal or nuclear is now a

matter of significant debate, as concerns over global warming have become

a major issue.

Despite concerns about possible restrictions on coal exports because of

increased domestic demand, new export collieries are being built. Earlier

this year, black empowerment company African Rainbow Minerals Ltd (ARM)

and Xstrata Coal announced the development of Goedgevonden, a new greenfield

open-pit, thermal coal mine.

When in full production, scheduled for 2011, Goedgevonden will produce

3.1 Mt/y of export thermal coal, along with 3.6 Mt/y for the domestic

market. Its life expectancy is estimated at 30 years. LAWS

HURT SMALL DIAMOND MINERS

As a whole last year, South Africa’s diamond production fell to 14.6

Mct, from 15.2 Mct. Whether this decline will be reversed significantly

by the arrival of new small producers is open to question. In part, this

fall in production is the result of legislation, which Mark Lotter, a

representative of the South African Diamond Producers’ Association

(SADPA), says is suffocating small-scale mining. This is because applications

for prospecting licences on properties covering more than 1.5 ha require

the same social and labour compliances from small miners as larger groups.

Lotter says small diamond miners cannot get bank loans unless they submit

a five-year business plan, which is difficult if miners do not have enough

land to prospect. Lotter believes the effect on small diamond miners has

been dramatic. In 2002, there were 1,000 operating diggers producing some

10% of South Africa’s diamonds. By 2006 their numbers were down to

164.

South Africa’s diamond industry remains in a considerable state of

flux as veteran producer De Beers closes some operations, reopens others

that were shut down a century ago and sells several others.

Essentially, De Beers wants to focus on its richest properties, the Venetia

and Finsch mines, and is reopening the Voerspoed mine in the Free State

at a cost of R1.2 billion (US$166,872). Voerspoed is expected to produce

700,000-800,000 ct/y by 2009 and have a life expectancy of 12-16 years.

De Beers is also busy initiating offshore mining off South Africa’s

west coast, although this has been sharply criticised by environmentalists,

who fear that it will cause as much damage to the seabed as the company’s

sea-mining operations in Namibian waters.

De Beers has not been alone in selling its poorer mining interests to

small and black empowerment operators. In March, Trans Hex Group Ltd sold

its Middle Orange River diamond operations to Rockwell Resources RSA,

(a subsidiary of Rockwell Ventures Inc of Canada) for R100 million. The

proceeds will be put towards its three more-profitable Lower Orange River

operations.

MIXED FORTUNES FOR FLUORSPAR

South Africa has about 10% of the world’s fluorspar reserves, but

its two principal producers have been experiencing mixed fortunes. Early

in 2007, the Spain’s Minerales y Productos Derivados SA (Europe’s

largest fluorspar user), invested R100 million in South African mining

junior Metorex Ltd and it is providing technical assistance for its Vergenoeg

fluorspar mine.

Metorex has been involved in a study into the possibility of establishing

an aluminium fluoride plant at Richards Bay to supply nearby aluminium

producers who currently import their fluoride needs. If the plant gets

the go-ahead, Vergenoeg’s annual production of fluorspar will increase

60,000-80,000 t/y from its current 180,000 t/y. Metorex’s principal

interest is supplying fluorspar to the new plant.

In contrast to Vergenoeg, which provides Metorex with some 15% of its

revenue at present, the Buffalo mine owned by Sallies Ltd has been plagued

wth difficulties. Some years ago Sallies tried, unsuccessfully, to renegotiate

a loss-making fixed-price supply contract with Honeywell. In good years,

when mining operations are not hampered by rains, Buffalo and the company’s

Witkop mine produce 200,000 t of fluorspar; about 5% of world demand.

Sallies and Honeywell have taken their dispute to international arbitration.

Meanwhile, Sallies posted a loss of R19,033 million last year.

GOLD’S LACK OF PROSPECTS

South Africa’s gold-mining industry remains in a state of long-term

structural decline. Annual production in 2006 was only slightly more than

a quarter of the 1970 peak and the lowest since the Witwatersrand miners’

strike of 1922. The declining trend persisted in the first half of 2007

as higher gold prices allowed the mines to process previously-marginal

ore.

Only the two majors, AngloGold Ashanti Ltd and Gold Fields Ltd, are engaged

in major deep-level developments and this is because there are few, if

any, prospects of new greenfield mines.

Gold Fields is focusing on deepening its Kloof and Driefontein mines at

a budgeted cost of R4.7 billion and bringing its South Deep project up

to full operation. South Deep was acquired from Western Areas Gold Mining

Co Ltd and Barrick Gold Corp at a cost of R3 billion in cash and shares.

An annual production target of 800,000 oz by the year 2011 has been set

for the mine, described as South Africa’s last large-scale gold resource.

According to Gold Fields’ chief executive, Ian Cockerill, the days

of new deep-level mines are over. While, according to his reckoning, some

800 Moz remain in the Witwatersrand Basin, the deeper one goes the more

patchy the reserves become.

AngloGold Ashanti’s development plans mirror those of Gold Fields:

deepening existing mines and extending operations into adjacent ground

– essentially brown-field operations.

By the beginning of this year, the company was looking into deepening

its South African mines in order to push an inevitable gold production

beyond the currently estimated five years. This would be in addition to

the current deepening of the TauTona and Mponeng mines.

The TauTona project will cost US$168 million and begin producing gold

in 2008 to yield 2.6 Moz of gold over nine years to 2017. The Mponeng

project will cost US$252 million, with production set to start in 2013.

The gold industry’s steady decline has resulted in older, marginal

mines being transferred to new owners, principally black-owned, who believe

they can exploit otherwise-unprofitable mines and have lower overhead

costs than the majors. They have also benefited from higher gold prices.

CAPACITY RISE TO BOOST MANGANESE

South Africa’s manganese sector, currently dominated by Assmang Ltd

and BHP Billiton’s Samancor Ltd, could soon see the advent of new

producers and beneficiation facilities if the hopes of black empowerment

and foreign entities are realised. An estimated 80% (350 Mt) of the world’s

manganese reserves are in southern Africa, but that does not give South

Africa any great leverage over the international market, which remains

over-supplied after growing demand from a buoyant world steel industry

led to an increase in prices almost two years ago.

Exxaro, in conjunction with Samancor, is examining the feasibility of

a 200,000 t/y ferromanganese facility based on completely new technology.

If successful, the new process could cut current ferromanganese production

costs by as much as a third.

Black empowerment group Kalagadi Manganese hopes to complete the feasibility

study for doubling capacity at its proposed new mine in the Northern Cape

province to 3 Mt/y. Just how these developments might affect the world’s

finely-balanced manganese market, currently oversupplied to the tune of

some 1 Mt/y, is another matter. Platinum on the way up The platinum industry

is in the throes of an unprecedented expansion. According to a platinum

conference held in July, if every expansion and new development plan reaches

fruition, an additional 4.5 Moz/y of platinum would be made available

to the market within five years.

There are, however, caveats. Speakers at the conference warned that, while

junior miners might count on using the excess smelter capacity of the

major producers for the time being, there could be capacity constraints

within five or six years. Furthermore, conference speakers warned that

the growth in demand might not match that of supply – a development

expected to lead to a fall in metal prices from their current level.

The industry is undergoing a restructuring of ownership as firms such

as Anglo Platinum sell off undeveloped or developing platinum assets to

black empowerment groups. Earlier this year, Anglo Platinum was anticipating

that platinum production would reach 2.8-2.9 Moz this year, but has scaled

back this estimate by 15,000 oz after a week-long closure of the company’s

Rustenburg mine to investigate the deaths of miners.

In parallel with the transfer of assets into black hands, there has been

a scramble to acquire developing properties. In August, Xstrata offered

US$1 billion to acquire junior miner Eland Platinum Holdings Ltd, which

is working to raise its annual refined-platinum output to 560,000 oz and

has been examining the possibility of further doubling capacity by end

2010.

Earlier this year, Lonmin plc acquired the Akanani platinum prospect from

AfriOre Ltd for US$450 million; a venture that Lonmin said is based on

thick reef with potentially high mining grades. Lonmin’s acquisition

was shortly followed by Implats’ US$600 million acquisition of AIM-listed

African Platinum plc, which has a single project, Leeuwkop, where mining

could reach depths of 1,300 m; particularly steep compared with the country’s

gold mines.

Leeuwkop is initially developing an open pit with an annual capacity of

160,000 oz of platinum, which could be lifted to 260,000 oz/y by going

underground. Eland owns the neighbouring Madibeng property, which it says

has resources that could take production to an annual 1 Moz of platinum

by 2015.

URANIUM

RENEWAL UNDER A CLOUD

Uranium prospects are looking very bright, according to promoters who

are developing or planning new mines. AngloGold Ashanti is, understandably,

less bullish than some newcomers. It is waiting for 2009 when contracts

at prices fixed at US$30/lb, less than a third of current spot prices,

expire and production as a by-product of gold is increased by a quarter

from its current annual 1.5 Mlb.

AngloGold Ashanti operates the only uranium production facility in South

Africa, a far cry from the last boom years of 30 years ago. The company

said in April that its annual uranium production might be increased by

60% to 1,100 t over the next few years, pending the outcome of a feasibility

report. The intention is to treat old slimes dams containing uranium tailings

at the Kopanang mine near the Vaal Reefs complex and upgrade treatment

facililties.

Gold Fields has also been considering how to turn the uranium in its mines’

slimes dams into a profitable substance, either by selling it or producing

uranium. However, the majors remain cautious, particularly over the possibility

of the uranium market correcting more quickly from its present stratospheric

spot-price levels than some expect.

Gold Fields has underground reserves at the Beisa property in the Free

State, but realises that restoring production of the nuclear metal is

not that simple. AngloGold Ashanti has also encountered technical problems

at its plants.

In May, First Uranium Corp increased its estimate of the net present value

of its Buffelsfontein operation to US$295 million from an earlier US$211

million. The higher valuation was based on an expected long-term uranium

price of US$50/lb and the acquisition of additional tailings near First

Uranium’s developing operations to process the veteran Buffelsfontein

gold mine’s own tailings.

The Buffelsfontein tailings are estimated to contain 42 Mlb of uranium

and 2.9 Moz of gold, and uranium production is scheduled to start in November

2008.

Toronto-listed First Uranium hopes to accelerate the commencement of production

at its Ezulweni project. Underground mining is scheduled to start in October,

with gold production set for April 2008 and uranium two months later.

Average annual production at Ezulwini for the life of the project to 2024

is expected to be 290,000 oz of gold and 888,000 lb of uranium.

Meanwhile, the Nuclear Energy Commission of South Africa has dusted off

investigations halted 15 years ago into the possibility of enriching uranium

for a new generation of nuclear reactors.